Private Credit at a Crossroads – Noise, Nuance, and the Resilience of Disciplined Lending

By Lucas Wüst, Founder & CEO at Kredo

The private credit market has come under intense scrutiny in recent months. Re-demption gates at major US funds, selective loan write-downs, and a series of stress scenarios circulating in the financial press have unsettled investors and prompted wide-ranging debate within the industry. This article draws on publicly available research to offer a measured assessment of what is actually happening and to reflect on what the current environment reveals about the enduring im-portance of sound credit fundamentals.

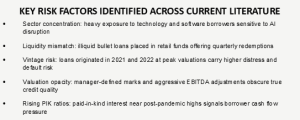

The turbulence in private credit stems from a specific and identifiable set of circumstances, not from a generalised deterioration of the asset class. The stress is concentrated in a handful of large US direct lending funds that built heavy exposure to technology and software companies, sectors now facing structural pressure from artificial intelligence disruption.

Blue Owl Capital became the focal point of concern after restricting redemptions in one of its retail-facing funds. Industry analysis converges on three compounding factors: overconcentration in AI infrastructure and tech-adjacent borrowers; the placement of inherently illiquid bullet loans into a fund with regular liquidity windows; and underwriting standards that proved inconsistent with the risk profile of the underlying assets. This is a story of structural mismatch and sector overexposure, not a signal of broad private credit failure.

Several institutions have noted that the episode has exposed real vulnerabilities in parts of the market: high leverage ratios, weak covenant packages, aggressive use of EBITDA add-backs, and limited transparency on valuations. These are legitimate concerns and they are, importantly, characteristics of a specific segment of the market rather than defining features of the asset class as a whole.

What the Data Actually Shows

Placing current defaults in context is essential. Fitch Ratings recorded a private credit default rate of 9.2% in 2025, up from 8.1% in 2024 and the highest for a full year on record. Under Fitch’s definition, a default occurs when a borrower fails to meet the legal obligations of a loan for any reason, a broad measure that encompasses covenant breaches and other technical events well short of actual payment failure. This figure must therefore be read alongside two more telling indicators. First, the ten-year average annual default rate for the asset class stands at around 2.6%, providing a more stable long-run reference point. Second, and more tellingly, non-accruals, being loans significantly past due where the borrower has stopped paying, represented only 0.6% of the original amount invested at the industry’s biggest fund, Blackstone’s $82.5 billion BCRED, and at Blue Owl’s OCIC as of the end of Q4 2025. They stood at 0% for Ares Management’s ASIF. The gap between headline default rates and realised losses reflects both definitional differences and the continued ability of lenders to manage distressed credits.

Leading private capital managers have signalled that default rates may continue to rise over the next few years, from a ten-year average of around 2.6%, as AI-driven economic transformation bifurcates borrower outcomes more sharply. Credit, by its nature, captures the full downside of business deterioration while capping the upside at contracted interest, making portfolio diversification and disciplined underwriting more important than ever.

A Market in Search of Transparency

One constructive response to the current episode has been an acceleration of efforts to bring greater transparency to the private credit market. According to the Wall Street Journal, several benchmark initiatives have been announced in recent months by providers including Lincoln International and S&P Dow Jones Indices, Kroll and StepStone, and Morningstar’s PitchBook unit, covering thousands of direct lending deals across the US and Europe. The aim is to give investors and fund managers the kind of comparative performance data that public markets take for granted.

The absence of robust benchmarks has long made it difficult to assess relative performance, identify concentration risks, and distinguish well-managed portfolios from poorly underwritten ones. As the market continues to mature and retail participation grows, this transparency gap is not merely a technical inconvenience but a structural vulnerability. Greater standardisation of reporting will strengthen the credibility of the asset class and support more informed capital allocation over the long term.

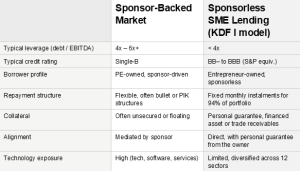

Sponsor-Backed Versus Sponsorless Lending: A Fundamental Distinction

Much of the current debate around private credit risk centres on the sponsor-backed segment, where loans are originated to private equity-owned companies typically carrying debt-to-EBITDA leverage of 4x to 6x or more, with credit quality often rated in the single-B range. This model has been the dominant growth engine of large-cap direct lending over the past decade and it is precisely this segment that is now under the most scrutiny.

Sponsor-backed transactions carry a distinctive risk profile. Private equity sponsors have optimised capital structures for return rather than resilience, meaning that borrowers often enter the lending relationship at the upper bounds of comfortable leverage. Covenants are frequently loose, EBITDA definitions are stretched, and the alignment between lender and borrower is mediated by a financial sponsor whose primary obligation is to its own investors. When sector conditions deteriorate, the consequences ripple through highly leveraged capital structures with limited margin for error.

Sponsorless lending, by contrast, extends credit directly to entrepreneur-owned businesses outside the private equity ecosystem. Borrowers are typically owner-managers with skin in the game, conservative capital structures built over years of organic growth, and businesses generating real, recurring cash flows. Leverage ratios are materially lower and the alignment between lender and borrower is direct, unmediated by any third-party financial sponsor.

The table below illustrates these contrasts, using Kredo Debt Fund I (KDF I) as a representative example of the sponsorless SME lending model.

This distinction matters enormously in the current environment. The risk of cascading defaults in private credit is, in large part, a risk of sponsor-driven leverage meeting sector disruption. Sponsorless SME lending is structurally insulated from both vectors: borrowers carry less debt, operate across non-correlated sectors with limited technology exposure, and bear direct personal accountability for their obligations. The risk profile is not merely different in degree but different in kind.

The Sponsorless Model in Practice: Kredo Debt Fund I

Kredo Debt Fund I (KDF I hereafter) illustrates how the sponsorless lending model translates into portfolio construction. Launched in July 2023, the fund lends exclusively to established Swiss SMEs: entrepreneur-owned businesses with stable, recurring cash flows, at least three years of operating history, and demonstrated debt service capacity. The portfolio carries no exposure to private equity sponsors or leveraged buyout structures.

Loan amounts range from CHF 50,000 to CHF 1 million. Monthly amortising term loans and asset-based lending facilities together represent approximately 94% of the portfolio and are repaid via fixed monthly instalments. Bullet loans, used for shorter-term transactional financing, carry terms of generally three to twelve months with principal repaid at maturity. Every credit is backed by tangible collateral: in the overwhelming majority of cases, the personal guarantee of the principal shareholder, and in the case of asset-based lending, a pledge over the financed equipment. This structure generates consistent and predictable cash flows at the portfolio level, directly supporting fund liquidity.

Sector exposure spans twelve industries including construction, healthcare, consumer and retail and ICT, with no single sector dominant. The ICT allocation is modest and, as with all borrowers in the portfolio, directed at established Swiss SMEs with recurring revenues. As with any diversified portfolio, individual positions may be affected by broader economic shifts, including those driven by technological change, and these are monitored accordingly. The weighted average probability of default across borrowers stands at 0.98%, equivalent to an S&P BB+ to BB rating. Since launch, the fund has delivered a net NAV progression of 11.76%, compared to 7.28% for the SBI Domestic Non-Government Mid Price 1–5 index over the same period.

KREDO DEBT FUND I – Selected portfolio metrics, January 2026

Source: KDF I Factsheet, January 2026

Conclusion: Selectivity, Not Retreat

The private credit market is not in systemic crisis. But the current episode has clarified important lessons. Concentration in sectors under rapid technological disruption creates fragility that diversification and conservative underwriting could mitigate. Liquidity mismatches between fund structure and underlying assets materialise under stress. Opacity in valuations erodes investor confidence in ways that become self-reinforcing.

For the digital lending industry, this environment is both a challenge and an opportunity. The challenge is that reputational spillover from distressed US funds is affecting sentiment toward the asset class broadly. The opportunity is that scrutiny of this kind reinforces the differentiated value of platforms that have built durable credit quality through rigorous borrower selection, genuine portfolio diversification, conservative leverage, and direct lender-borrower alignment, the defining characteristics of sponsorless SME lending.

The principle is straightforward: selectivity over breadth, quality over yield maximisation, and borrower alignment over financial engineering. Discipline, in this environment, is not a constraint on returns. It is the precondition for them.

This insight was published in the DLA Quarterly Briefing No 1/26 on May 8, 2026. It can be downloaded here.

The author writes in a personal capacity as Founder & CEO of Kredo Ltd.

Photo Credit:

- Lucas Wüst: Kredo Ltd.

Sources:

- WSJ, „New Benchmarks Aim to Pierce Opaque Private-Credit Market“ (24 February 2026);

- WSJ, „What Private-Credit Investors Need to Know About the Industry’s Turmoil“ (13 March 2026);

- Partners Group / Financial Times, „Partners Group sounds alarm on private credit default rates“ (12 March 2026);

- UBS CIO Weekly Global (23 March 2026);

- Kredo Debt Fund I Factsheet (January 2026). All fund data sourced from the KDF I Factsheet.

Please note:

The content of this insight is expressly not to be considered investment advice, but is intended solely for your information.